Bluevine Review

Business checking with paid interest tiers, plus lines of credit and term loans

Is this your product? Claim this page · Request a change

Looking for a Bluevine alternative? See our ranked comparison.→What is Bluevine?

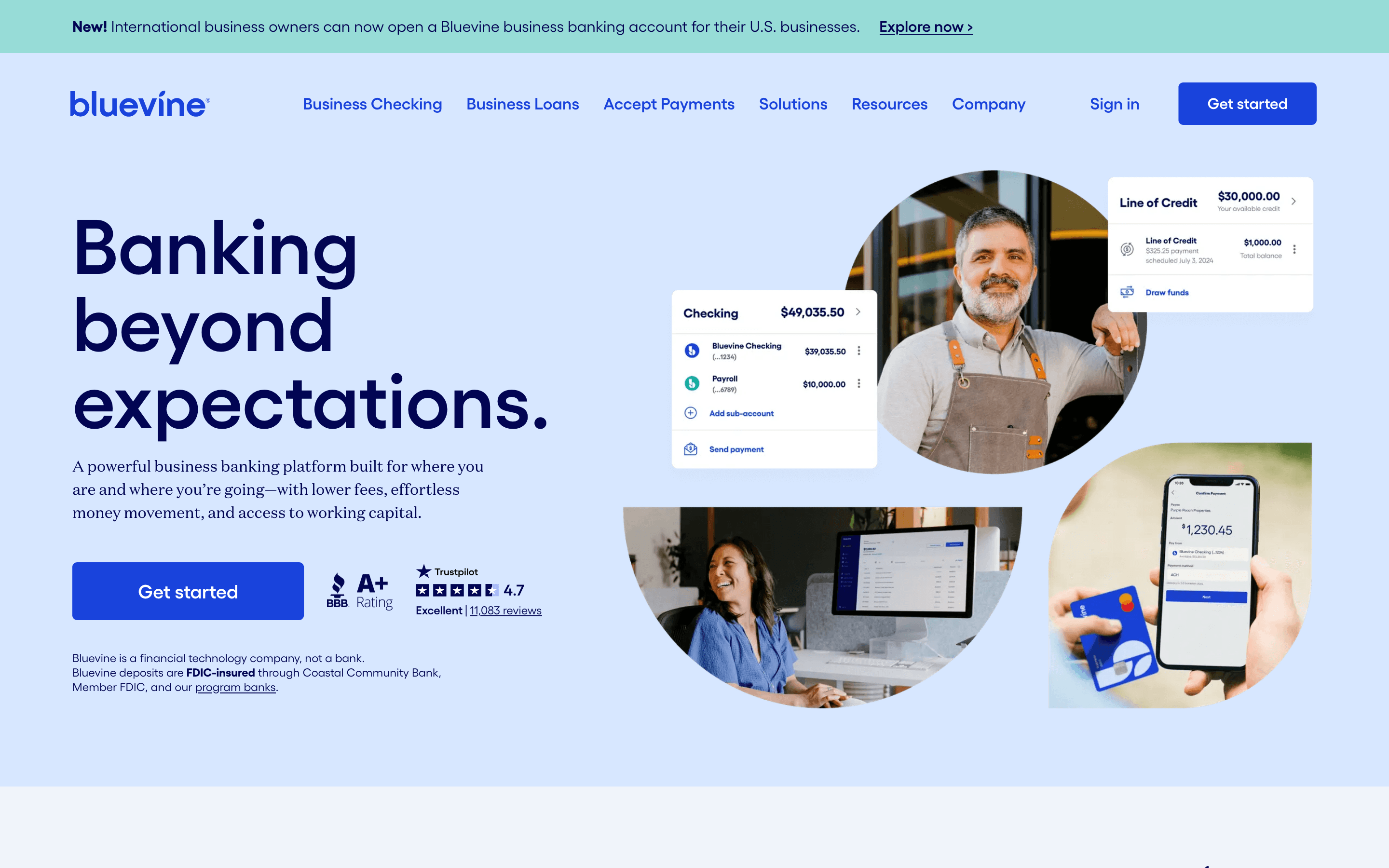

Bluevine is an online business checking account that pays interest, plus a line of credit and term loans for working capital. It is not a chartered bank itself. Deposits sit at partner banks (Coastal Community Bank and others) and are FDIC insured up to $3 million by spreading balances across them.

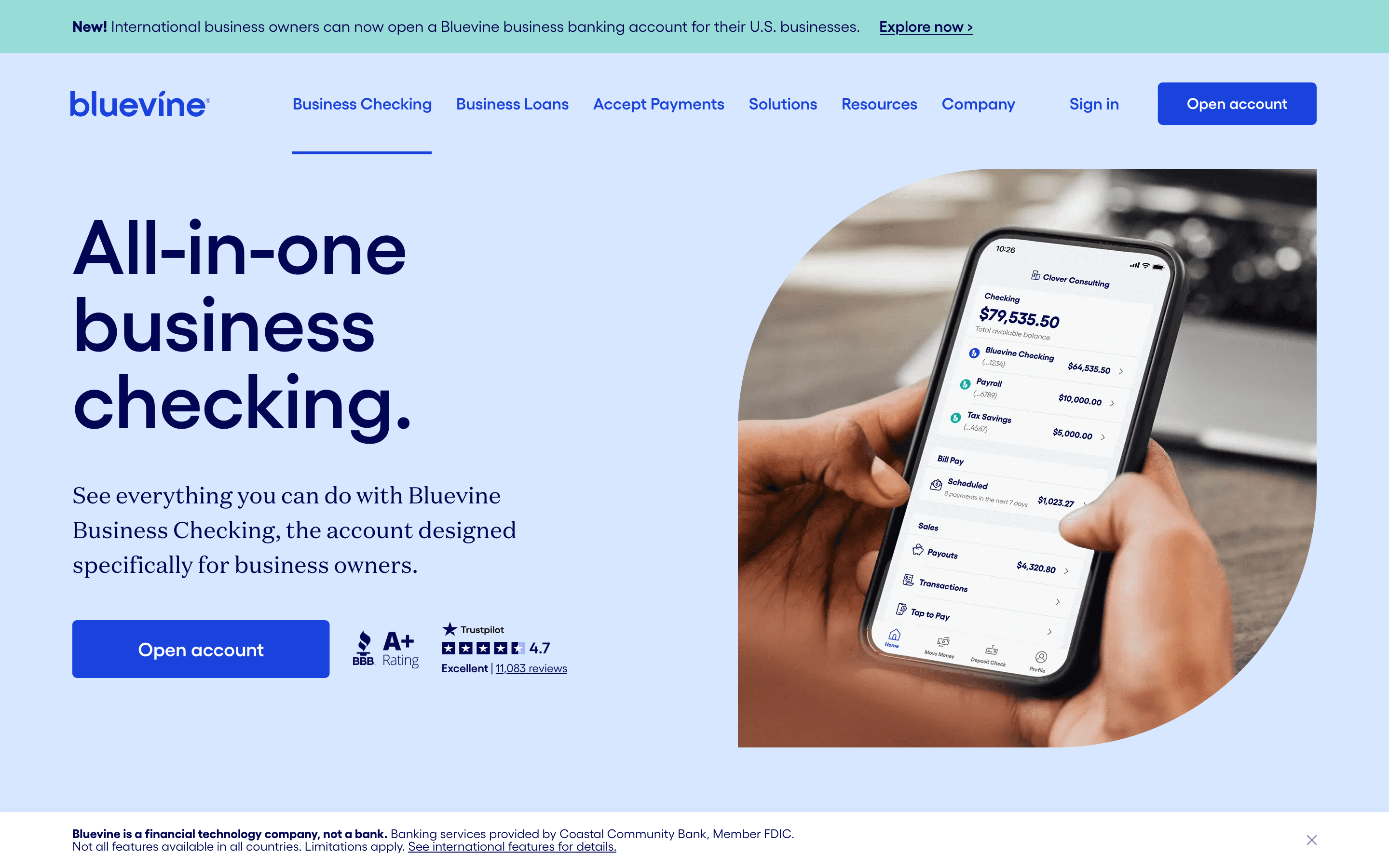

The checking product has three tiers. Standard is free but only earns 1.3% APY if you hit a monthly spend or deposit minimum. Plus and Premier charge a monthly fee and pay more interest with no strings attached, topping out at 3% APY on Premier with no balance cap. Bluevine has also added invoicing, payment links, and Tap to Pay so you can collect from customers without a separate tool.

Bluevine screenshots

Who it's for

- ✓ Businesses that want a free checking account and don't mind meeting a small monthly spend or deposit minimum to earn interest

- ✓ Businesses that want to earn a real yield on a working cash balance without moving it to a separate savings product

- ✓ Businesses that also want a line of credit or term loan from the same provider

Who should look elsewhere

- ✗ Businesses that need weekend or after-hours support if something goes wrong with the account

- ✗ Businesses that can't tolerate a hold or freeze while an account is under review

- ✗ Businesses that want one flat free plan with no tiers or interest conditions to track

Pros

- + No monthly fee and no minimum balance on the Standard plan

- + 3% APY on the Premier plan applies to the full balance with no cap

- + FDIC coverage up to $3 million by spreading deposits across partner banks

- + Line of credit and term loans available from the same account

- + Invoicing, payment links, and Tap to Pay now built in, so you don't need a separate invoicing tool

Cons

- – Earning interest on the free Standard plan requires hitting a monthly debit spend or deposit minimum

- – Support hours run Monday through Friday, 8am to 8pm ET, with no stated weekend hours, so a Friday account freeze can mean waiting until Monday

- – Multiple customer reports of accounts frozen or funds held for weeks during account reviews, with little explanation given

- – Plus and Premier monthly fees are billed unless waived, and the site doesn't spell out the waiver terms up front

Bluevine pricing

It has a free plan, so you can start at no cost in Startup Banking.

| Plan | Price | Highlights |

|---|---|---|

| Standard | Free | No monthly fee · 1.3% APY up to $250,000 · Requires $500/month on the debit card or $2,500/month in deposits to earn interest |

| Plus | $30/mo | $30/month fee, waivable · 1.75% APY up to $250,000 · No spend or deposit requirement to earn interest |

| Premier | $95/mo | $95/month fee, waivable · 3.0% APY on all balances, no cap · ACH positive pay and other fraud controls |

Checking has no monthly fee on the Standard plan and no minimum balance on any plan. Plus and Premier charge a monthly fee that Bluevine says is waivable, though the site does not spell out the waiver condition on the pricing page itself. Outgoing wires run up to $15, same-day ACH up to $10, paper checks $1.50 each, and international payments up to $25 plus about 1.5% in currency conversion. Bluevine also sells a business line of credit up to $250,000 and term loans up to $500,000 through partners, both priced case by case and not listed publicly.

Pricing verified July 7, 2026 · source

How Bluevine's pricing compares

Bluevine next to its closest alternatives on entry price, billing, and whether pricing is public.

Is Bluevine still actively developed?

Last significant update: February 2026. Added estimates that convert into invoices, service charges and discounts on invoices, multi-business account switching with instant free transfers between a user's own Bluevine accounts, and ACH positive pay for Premier customers.

Top Bluevine alternatives

Bluevine FAQ

Is Bluevine business checking free?+

The Standard plan has no monthly fee, but you only earn its 1.3% APY if you spend $500 a month on the debit card or deposit $2,500 a month. Plus and Premier charge a monthly fee (waivable) in exchange for higher interest with no spend requirement.

How is Bluevine FDIC insured if it isn't a bank?+

Bluevine is a fintech, not a chartered bank. Deposits are held at partner banks including Coastal Community Bank, and Bluevine says balances are swept across enough partner banks to cover up to $3 million per depositor, well above the standard $250,000 FDIC limit at a single bank.

What happens if Bluevine freezes my account?+

Multiple customers report accounts placed under review or frozen with little explanation, and funds held for a week or more during verification. Bluevine's own help center lists support hours as Monday through Friday, 8am to 8pm ET, with no weekend hours stated, so a freeze late in the week can mean waiting until the next business day to start resolving it.

Does Bluevine offer loans, not just checking?+

Yes. Bluevine offers a business line of credit up to $250,000 and term loans up to $500,000 through lending partners, both underwritten and priced individually rather than listed at a fixed rate.